EV adoption in India is happening at a faster pace than you think

- Published

- Reading Time

- 2 minutes

- Contents

When Arpit and I first released our first-ever EV Primer in April 2022, it was driven by the need to summarise our learnings from being long-term investors in companies such as Yulu, Euler, BatterySmart, ElectricPe and Vecmocon. It allowed us to engage with the EV (and auto) ecosystem. With the release of the second version, we now aim to capture how the last year has been for EVs in the country regarding OEMs, charging, financing, and auto components. We added two additional sections on EV distribution and battery recycling for our latest edition.

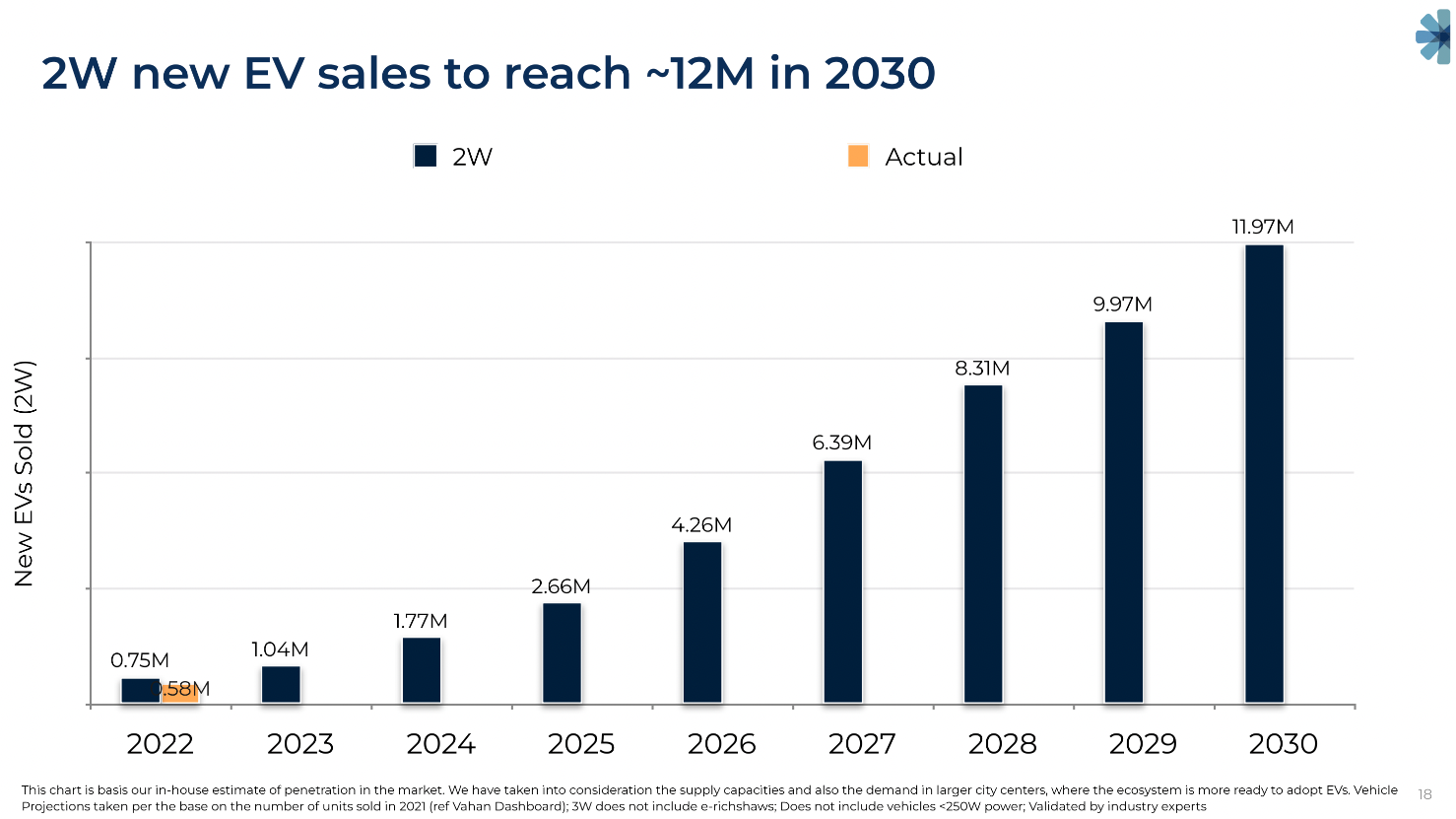

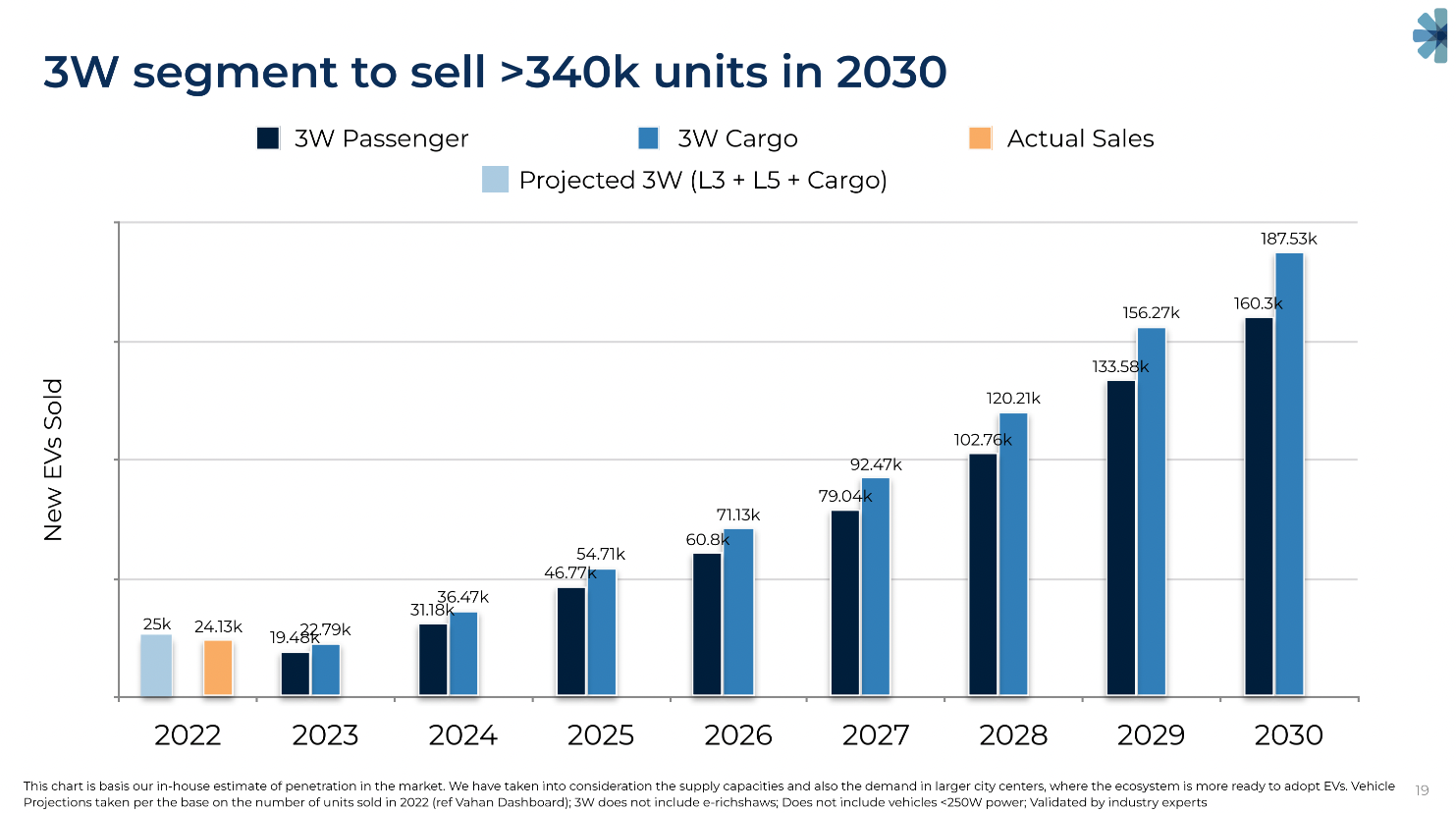

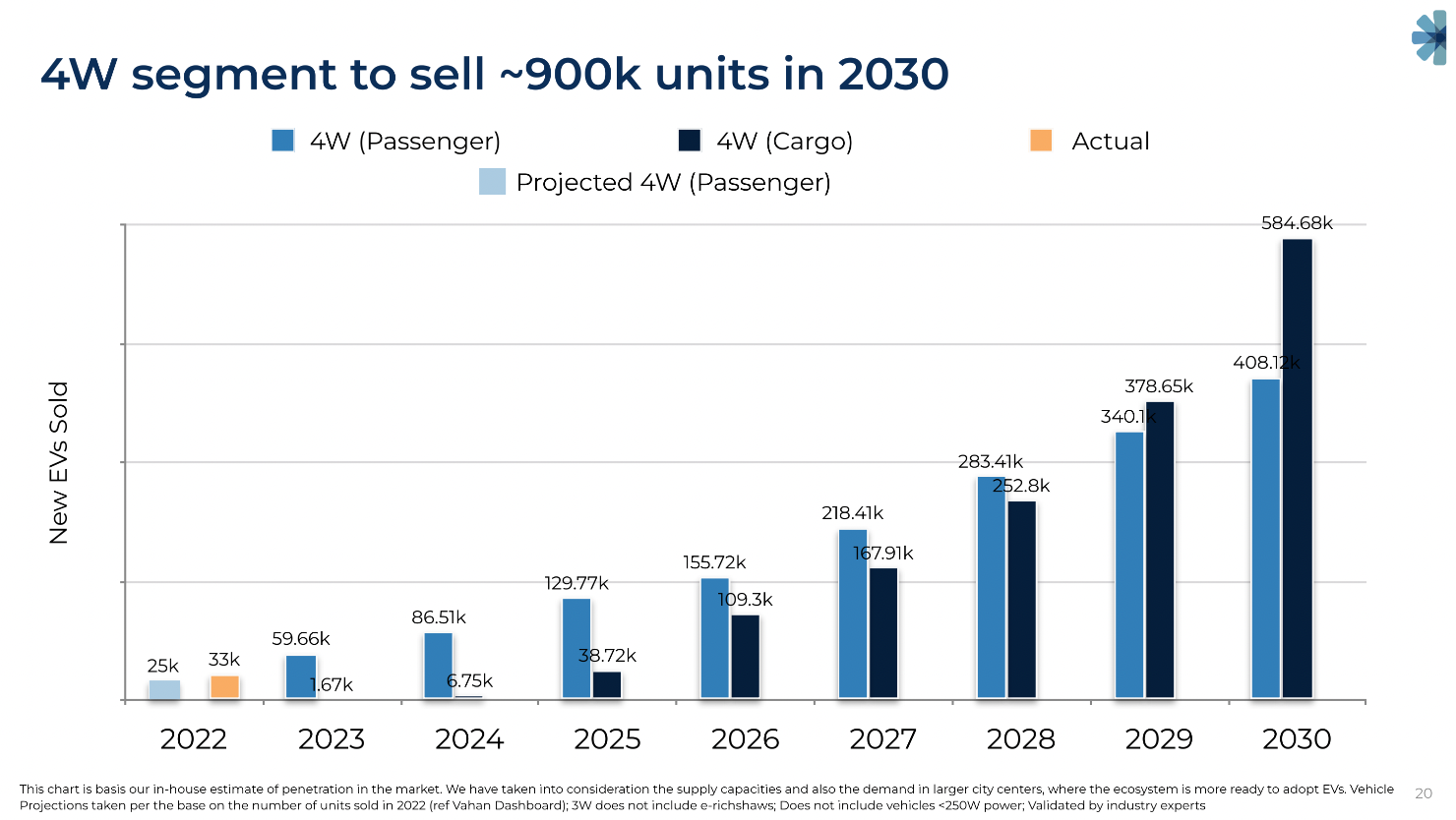

Let’s start with some good news. Our estimates for 2W, 3W and 3W sales have been 77%, 96% and 68% accurate! However, in some instances, we have rationalised our EV sales projections across some segments due to feedback from the ground.

Evolving Ecosystem

A few key things have happened over the last year in the EV industry:

- Introduction of AIS 156 standard;

- Reduction of FAME II subsidies for 2Ws (starting June 2023),

- Spike in Li-Ion battery prices in 2022,

- A drastic change in the availability of suitable vehicles, components and financing for EVs.

While the AIS 156 aims to increase vehicle safety, it has led to OEMs having to design their vehicles, build new partnerships and further re-certify them! This phenomenon has led to a prolonged growth of EV sales in the first half of 2023! FAME II subsidies have now been reduced starting June 2023 for 2Ws, leading to May 2023 recording 1L+, the highest number of 2Ws ever sold in the country.

Except for buses, all of the segments of EVs are now TCO-positive, which means we should expect a very high penetration rate going forward. Ather vehicles are now available with interest rates as low as 5.99% from large banks such as IDFC First. It has been one of the most significant positive changes, which makes us believe there would be further reduction in TCO across other segments.

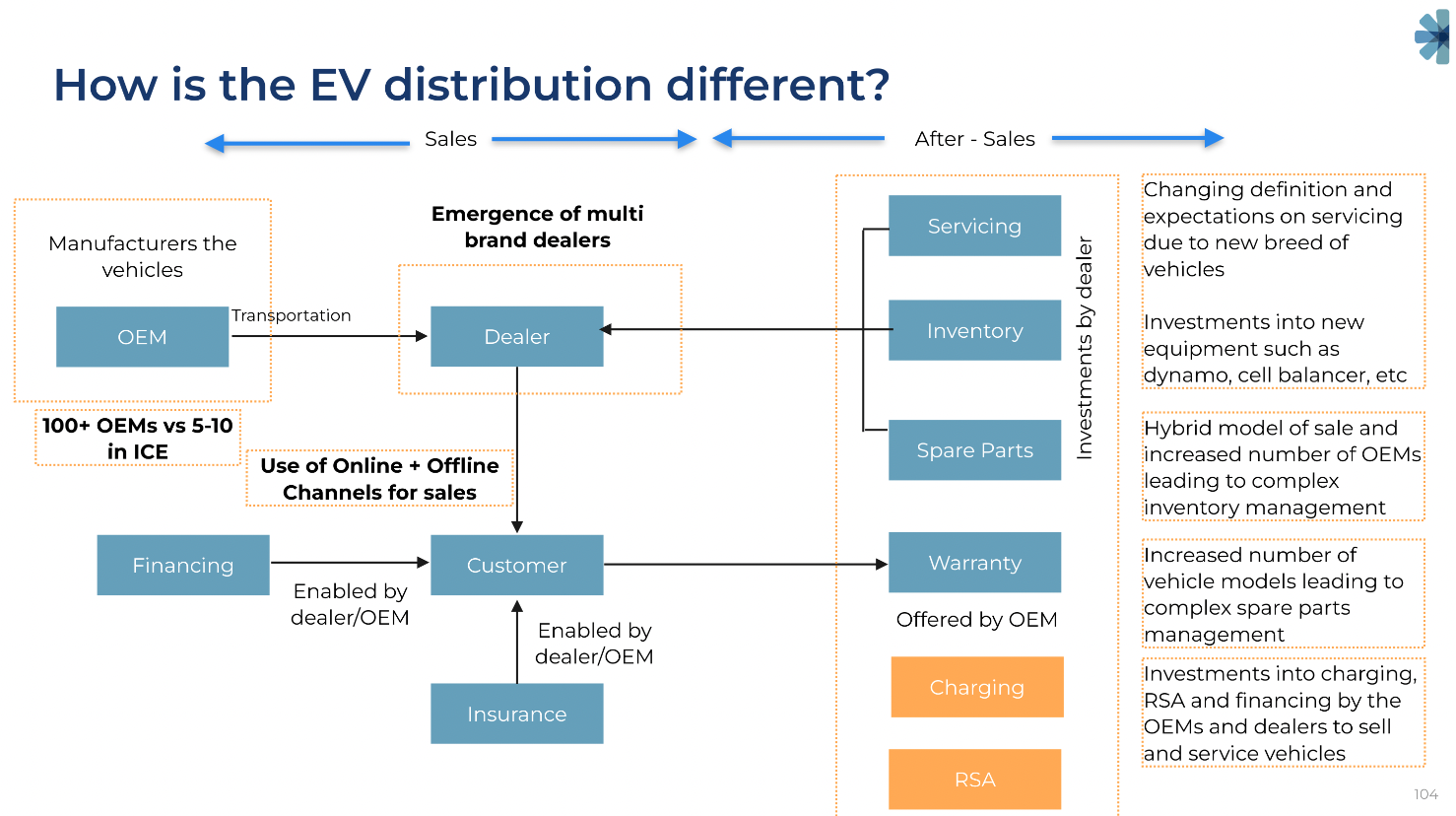

EV distribution businesses are a key focus area

We are observing a rise in EVs’ new-age distribution models. Given the software-first approach and mix of channels, the EV distribution business is very different from ICE distribution. Multi-brand outlets and enterprises have emerged. A key differentiator is the enhanced focus on servicing.

Arpit and I have been bullish and optimistic about the rise of EVs in the country. Slowly, steadily but surely, EVs will be mainstream throughout the country! We hope the second version of this report helps any founder, VC, or industry stakeholder navigate the complexities of multiple business models!

Here’s the link to the report — www.evprimer.in

Topics

Authors

Arpit Agarwal

Arpit is a Partner at Blume Ventures from Investment Team. He is amongst the most passionate people in India on enabling startups. He co-founded Headstart Network, India's largest startup community which touches more than 100,000…- Current Section

- Partner

- Sector

- DeepTech, ClimateTech, EV & Mobility, Healthcare, Logistics

Venkatesh Modi

Venkatesh has come full circle from being an intern at Blume in 2017 to an investment team analyst in 2020. Based in Bangalore, he overlooks climate tech, EV, mobility, deeptech and healthcare sectors at Blume. Before this, Venkatesh…- Current Section

- Associate

- Sector

- Healthcare, Logistics, EV & Mobility, DeepTech

Commentaries

Decoding The Indian Deep Tech Startup Ecosystem: Arpit Agarwal talks to Pronojit Saha on the Deep Tech Musings Podcast

Republished from the Deep Tech Musings podcast with permission. Listen now on - Spotify,- Current Section

- Commentary

- Sector

- ClimateTech, DeepTech, EV & Mobility, Logistics

- Published

Charging Towards A Solution: Why EVs Need Both Slow And Fast Charging Infra

Any discussion about EVs is incomplete without discussing how we power the vehicle. Do we swap batteries or use a charging station? The obvious but unhelpful answer is whatever gets you to from point A to point B at an optimal speed and…- Current Section

- Commentary

- Sector

- ClimateTech, EV & Mobility

- Authors

- Arpit Agarwal

- Published

Winning In The Two-Wheeler EV Market In India

Last few years saw over two dozen startups trying to make a mark in the e-mobility space, many of them run by fresh engineering graduates. E-mobility was a blank space ripe for disruption. Swiggy and Zomato did something similar when…- Current Section

- Commentary

- Sector

- ClimateTech, EV & Mobility

- Authors

- Arpit Agarwal, Disha Sharma

- Published

The Road To Electric Vehicles: A Primer To Decode The Ecosystem

By Arpit Agarwal, Venkatesh Modi We have been closely following the EV space for years, especially since it gathered steam four years ago. Over time, we garnered enough takeaways to compile into a single account – the only…- Current Section

- Commentary

- Sector

- EV & Mobility

- Authors

- Arpit Agarwal

- Published