The Age of Intelligent Finance Bluprint (Part II)

- Published

- Reading Time

- 3 minutes

- Contents

This is Part II of a two part series that explores the intersection of fintech and AI. For Part I, click here.

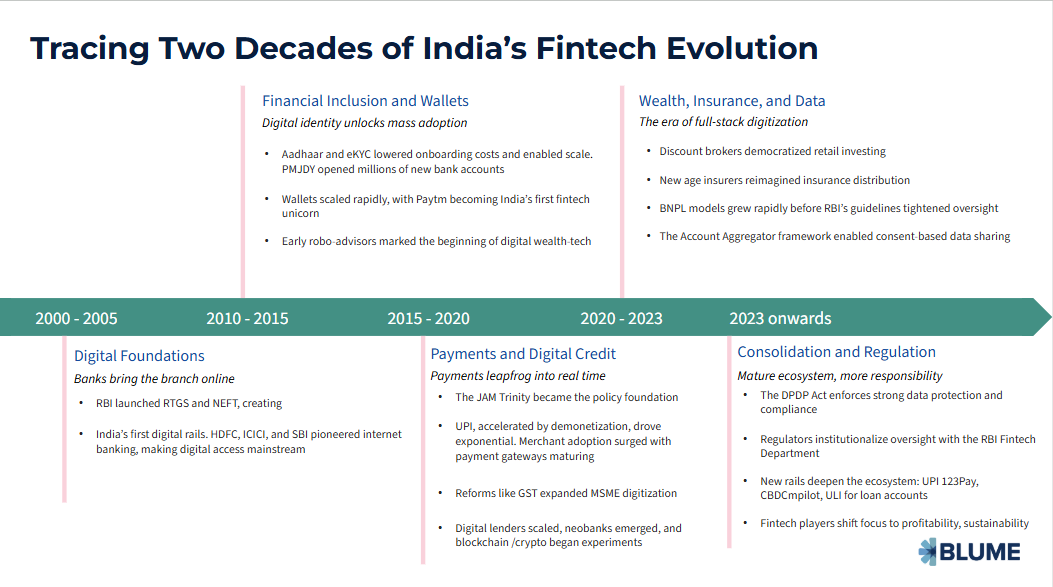

For over a decade, India’s fintech story was about building rails — Aadhaar gave identity, UPI made money instantly, Account Aggregators promised consented data etc.

Together, they unlocked access at a scale no other market had seen. Payments became invisible. Credit and investing moved online. For millions, simply entering the financial system was the win.

But something fundamental is shifting…

Access is no longer the problem. Decision-making is. Users are inside the system — but alone with dashboards, choices, and risk.

At Blume, we’ve been watching how AI is quietly changing at this moment. We’ve spoken to founders building conversational finance, insurers automating claims end-to-end, lenders underwriting from behavior instead of scores, and incumbents embedding generative models deep into their stacks etc. Across these conversations, a pattern kept repeating —

AI wasn’t just improving workflows. It was becoming the intelligence layer of finance itself.

What began as back-office automation is now shaping how people save, borrow, insure, and invest — in real time, in context, and in language they understand. Static products are turning adaptive. Transactions are becoming relationships. Finance is learning to respond.

This thesis explores that transition — from access to outcomes, from products to systems, and from digital finance to intelligent finance.

To read the full thesis, click here.

India made great progress in access/reach. Intelligence is the next frontier.

Over the last decade, India built one of the world’s most powerful fintech foundations.

Digital public infrastructure — Aadhaar, UPI, Account Aggregators — unlocked scale, inclusion, and participation at population level.

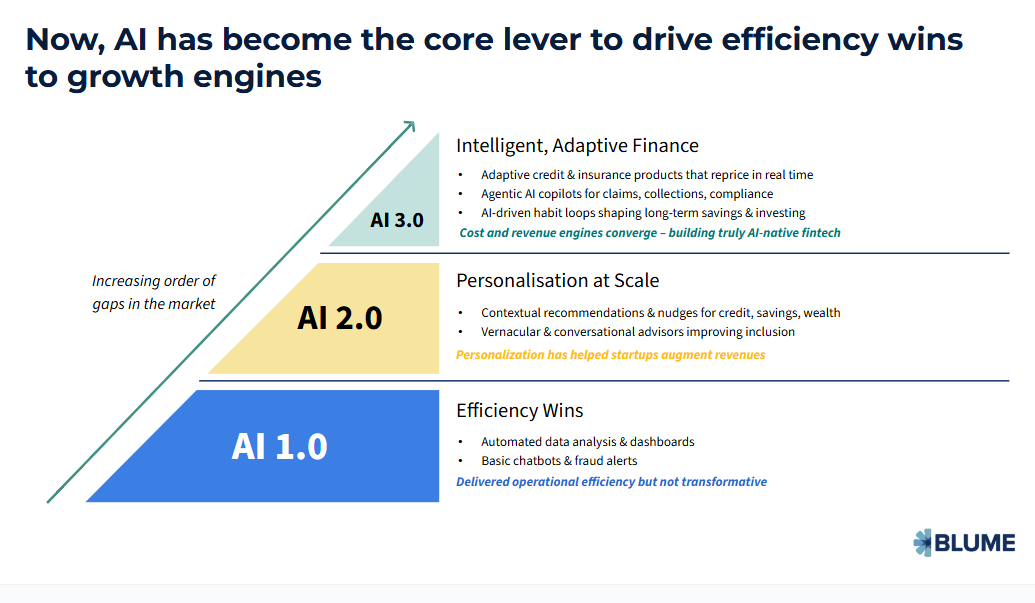

But as fintech matures, access alone is no longer the constraint. The next leap is being driven by intelligence — systems that understand context, adapt in real time, and guide users through complex financial decisions. We are entering the Age of Intelligent Finance, where AI moves from back-office efficiency to the core driver of personalization, trust, and growth.

From products and dashboards to adaptive financial systems

Most fintech products today still behave like static tools: Dashboards instead of guidance, Annual advice instead of continuous intelligence, One-size-fits-all products instead of context-aware experiences. AI changes this fundamentally. Generative and agentic AI are transforming fintech from transactional interfaces into adaptive systems — capable of real-time underwriting, conversational advice, dynamic pricing, and habit-forming financial journeys.

This shift matters because financial outcomes are behavioral, not informational.

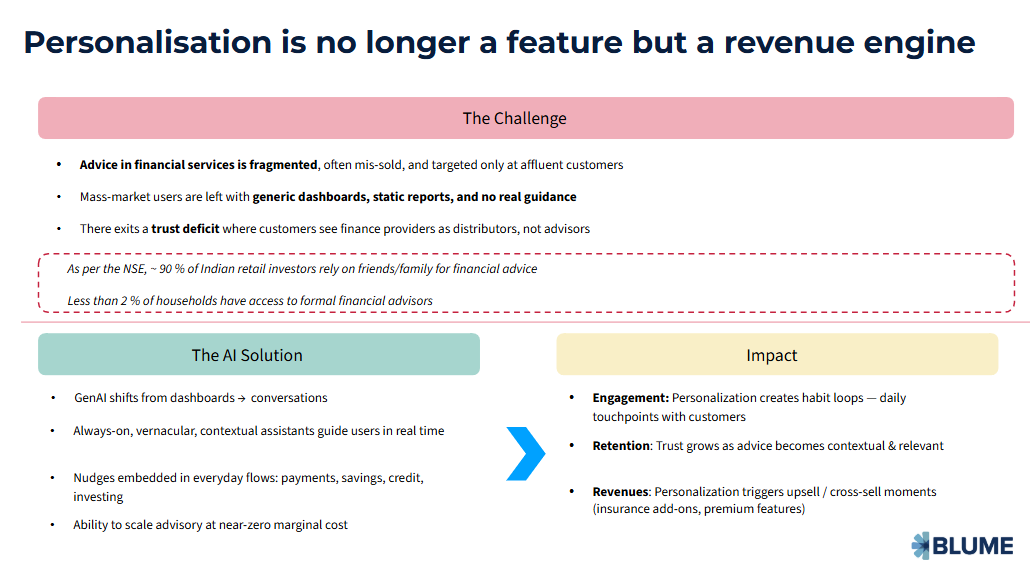

Personalization is no longer a feature — it is the business model

In India today: ~90% of retail investors rely on friends and family for advice, <2% of households have access to formal financial advisors.

AI enables advisory to scale at near-zero marginal cost — not as static reports, but as always-on, vernacular, contextual conversations embedded into everyday flows like payments, savings, credit, and investing. The result is not just better UX: Higher engagement through habit loops, Stronger retention via trust, Monetization through contextual upsell and cross-sell. Personalization is becoming fintech’s primary revenue engine.

So, where do we see opportunities?

Across wealth, insurance, and credit, AI is unlocking operating leverage at scale: Wealth: From static portfolios to continuous intelligence loops, Insurance: From paperwork-heavy claims to real-time, data-driven flows, Credit: From bureau-based scoring to behavioral, cash-flow underwriting.

What’s changing is not just cost structures — but how financial products are designed, priced, and delivered. The biggest opportunities are probably not “another fintech app”. They sit in infrastructure, interfaces, and trust layers — built invisibly into existing user journeys.

- Embedded finance (where intent already exists) — The fastest-growing financial actions will happen outside traditional fintech apps — inside commerce, mobility, gig, SaaS, and super-app flows. Embedded finance is growing faster than ever, but the intelligence layer is still thin.

- Behavioural + Vernacular AI as the new trust layer — India’s next 500M users don’t need more information — they need guidance they trust.

- Infra-first plays beneath the app layer — Some of the most durable value will accrue to unsexy, infrastructure-heavy companies that power many frontends.

The winners of this next phase won’t be defined by distribution alone, but by their ability to build invisible, intelligent, and trusted financial infrastructure. This is the age of intelligent finance — and it is just beginning.

Author

Udayan Pandey

Udayan focuses on Fintech investments within Blume and is based out of Mumbai. He has spent last 10 years in Financial Services space and has a diverse work experiences in EMEA and Indian markets. He is a Founder of a supply chain…- Current Section

- Vice President, Investment

- Sector

- FinTech