The Age of Intelligent Finance: The Personalization Playbook

- Published

- Reading Time

- 3 minutes

- Contents

This is Part 1 of a two part series that explores the intersection of fintech and AI

In 2022, ChatGPT sprinted from zero to one million users in under a week. Today — depending on whose numbers you believe — it serves between 600 and 800 million people every week. We already trust large language models to debug code, plan holidays, and draft legal letters. The question is no longer if we’ll trust AI to answer something far more delicate—“What should I do with my money?”—but when.

This leap will not happen in a vacuum. It’s being shaped by the realities of personal finance in India today — realities that make the need for a trustworthy, personalised financial guide more urgent than ever.

The Problem: Access Without Understanding

India’s digital finance story is, on paper, a success. UPI payments have overtaken credit card swipes. Aadhaar allows instant identity verification. The India Stack has enabled near-instant account openings and paperless onboarding.

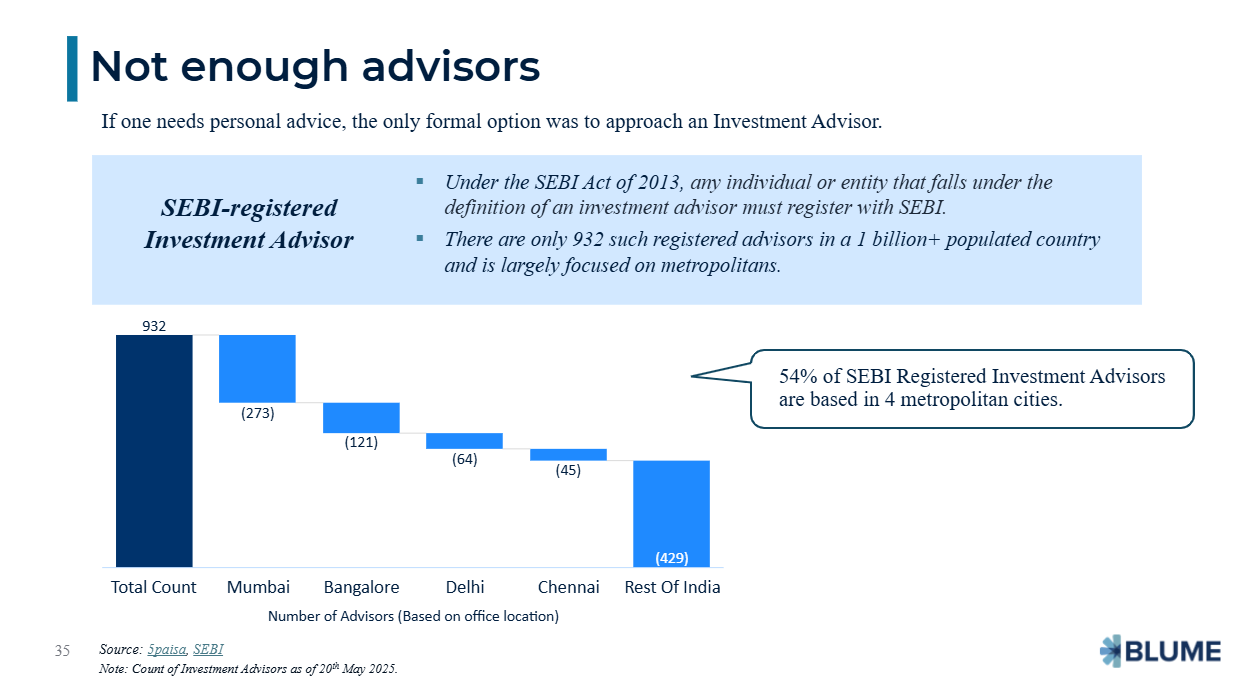

Yet these achievements mask a more uncomfortable truth: financial literacy has barely moved in a decade. Only 35% of adults understand the basics of saving, borrowing, and investing. And with fewer than 1,000 registered investment advisors serving a country of 1.4 billion — half of them concentrated in just four cities — most people simply have no access to reliable, professional guidance.

Into this vacuum has rushed a tide of mis-selling. Insurance products masquerade as investments. Credit cards arrive unasked for, bundled with fees hidden in fine print. Predatory lenders promise instant credit while charging crippling interest rates. The damage is systemic: 57% of relationship managers admit to mis-selling products to meet targets, and 84% say they operate under intense sales pressure. Most victims never even realise they’ve been mis-sold to, so complaints remain vanishingly rare.

The outcome is predictable. India has achieved financial inclusion in terms of access, but not in usage. People can open accounts, take loans, and invest in funds — but too often, they do so without the understanding to make these decisions work in their favour.

Why Now: The Infrastructure Is Ready

Two forces are aligning to change this: the maturation of India’s digital public infrastructure, and the rapid evolution of AI.

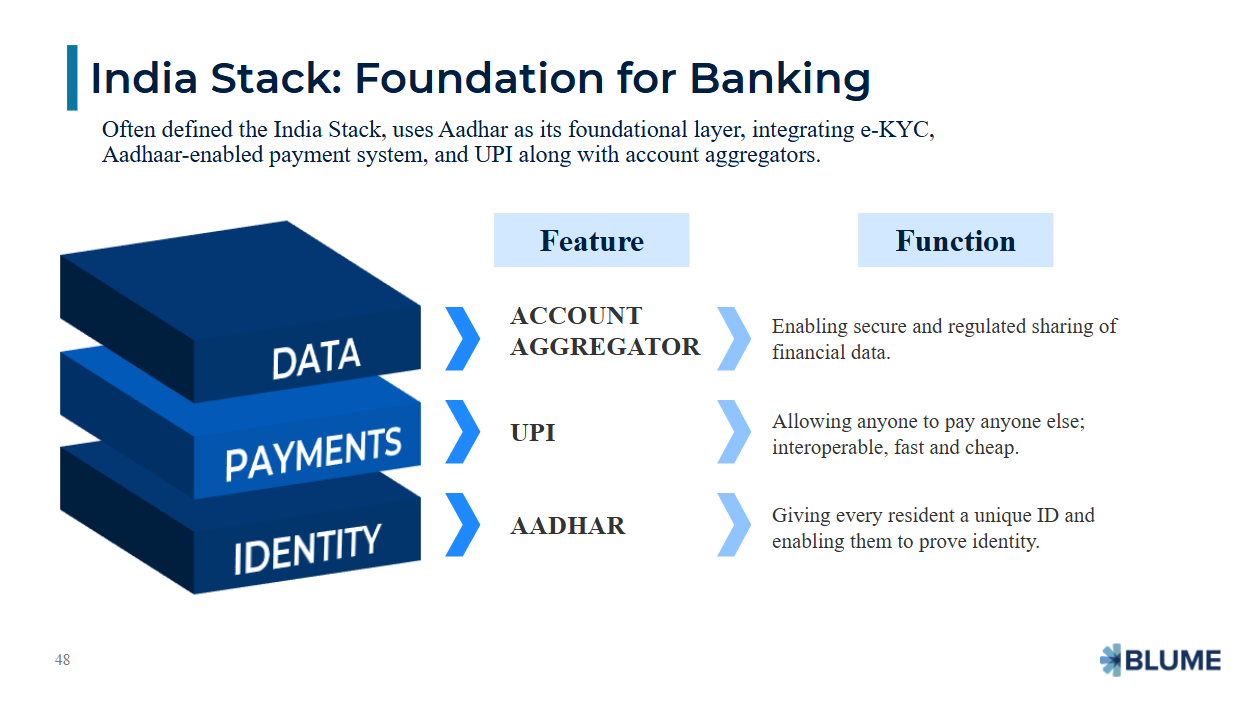

The Account Aggregator framework is quietly revolutionising how financial data moves. With a single digital consent, an individual’s bank statements, insurance policies, and investments can be securely pulled together into one unified profile. No more files scattered across inboxes and cabinets — this is structured, machine-readable data ready to be acted upon.

As of now, more than 212 crore accounts are live on the AA framework, with 100% coverage of demat accounts, pension accounts, and GSTIN taxpayers. Over time, all financial accounts will be connected, creating a comprehensive, real-time view of an individual’s financial life.

On the other side of the equation, AI — especially large language models — is reaching a point where it can interpret that data and translate it into advice that feels human, but is infinitely more scalable. An AI-powered coach could look at your cash flow, flag a debt trap before you fall into it, recommend products aligned to your goals, and nudge you towards healthier financial behaviour — not in broad, generic strokes, but in a way that reflects your exact circumstances.

The Shape of What’s Coming

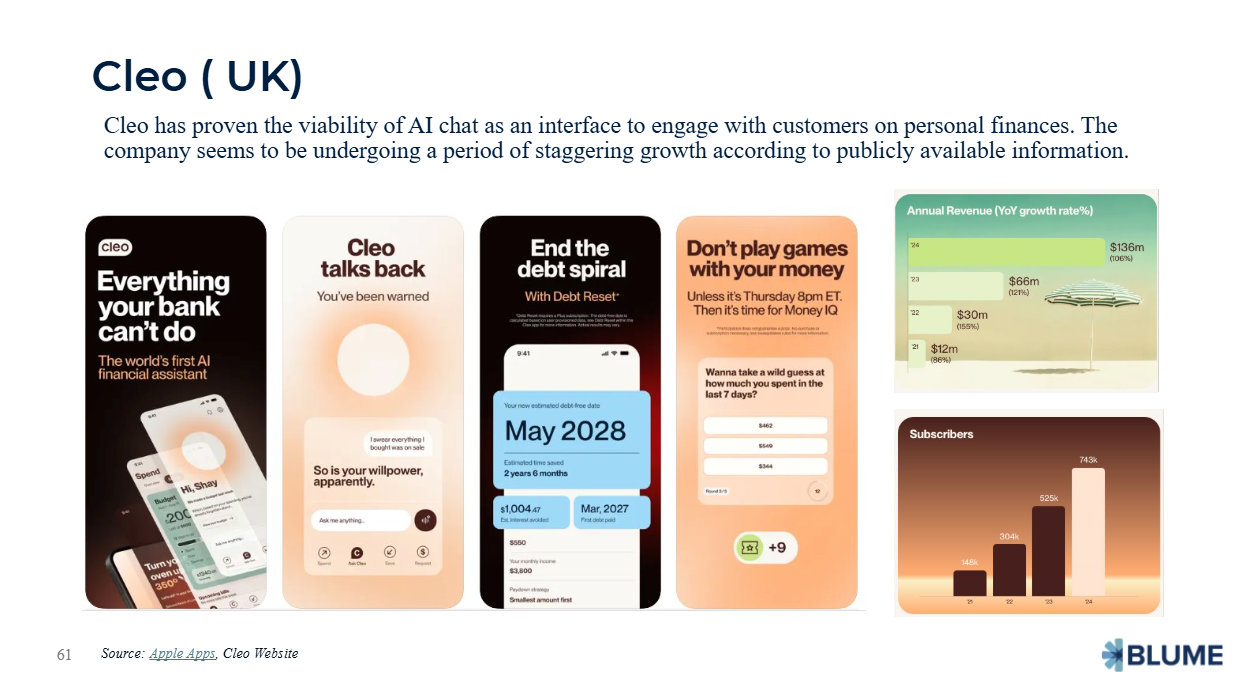

Early glimpses of this future are already visible. In personal finance, apps like Cleo and Peek AI are experimenting with conversational assistants that can analyse a user’s finances in real time in more advanced markets.

The direction is clear: the most valuable financial platforms of the next decade won’t just be marketplaces for products — they will be companions, embedded into your financial life, anticipating your needs, and steering you away from harm.

This isn’t without its challenges. AI “hallucinations” can be dangerous in finance, and privacy safeguards must be ironclad. But the building blocks are here: unified data rails, increasingly capable AI models, and a consumer base that is already comfortable interacting with digital assistants.

The Opportunity

The opportunity to build here is immense. A well-designed AI finance coach could serve hundreds of millions without the constraints of human advisor capacity. It could level the playing field — making personalised, conflict-free advice available to the first-time investor in Kattapana as easily as to a seasoned professional in Koramangala.

If India’s first wave of digital finance was about access, the next wave must be about trust. Embedding personalised, unbiased advice into the very fabric of financial services could unlock a “trust dividend” that reshapes how India saves, invests, and prospers.

The timing could not be better. The rails are built. The AI is ready. The need is undeniable. The question now is: who will build the companion that India can trust with its financial future?

To read the full thesis, please click here

Author

Joseph Sebastian

Joseph covers the logistics, fintech and healthtech sectors at Blume. Prior to joining Blume, Joseph was an impact investor at Omidyar Network India.He has extensive experience across the financial services domain first as a…- Current Section

- Vice President, Investment

- Sector

- Healthcare, Logistics, EV & Mobility, DeepTech, FinTech, ClimateTech

Commentaries

How to Evaluate Voice AI Platforms (Without Getting Lost in the Hype)

This is a guest post by Apurv Agrawal, Co-founder and CEO of SquadStack.ai, a Blume Fund II portfolio company. Search got solved. Coding is getting eaten by models. Now we’re…- Current Section

- Commentary

- Sector

- Artificial Intelligence

- Authors

- Apurv Agrawal

- Published