Lab Grown Diamonds Bluprint

- Published

- Reading Time

- 4 minutes

We all grew up listening to how “diamonds are forever.” De Beers didn’t just sell stones — they sold permanence, rarity, and emotional weight. For decades, that narrative shaped how India thought about jewellery: gold for security, diamonds for milestones, and both tied deeply to perceived investment value.

But something fundamental is shifting.

At Blume, we’ve been tracking lab-grown diamonds for a while now. We’ve spoken with miners, retailers, manufacturers, brands, growers and consumers. We’ve even witnessed LGDs growing in their surreal pink hue inside CVD chambers. We’ve stood outside stores, speaking to customers as they moved from one brand outlet to another. These conversations and observations shaped our understanding more than any single dataset. They revealed that LGDs aren’t solving for “cheap diamonds”, they’re solving for optionality, frequency, and self-expression.

What started as a niche curiosity has quietly become a genuine market shift, not just in what people buy, but in how they think about jewellery altogether.

To read the full Bluprint, please click here

The Consumer is Changing And So is the Purchase

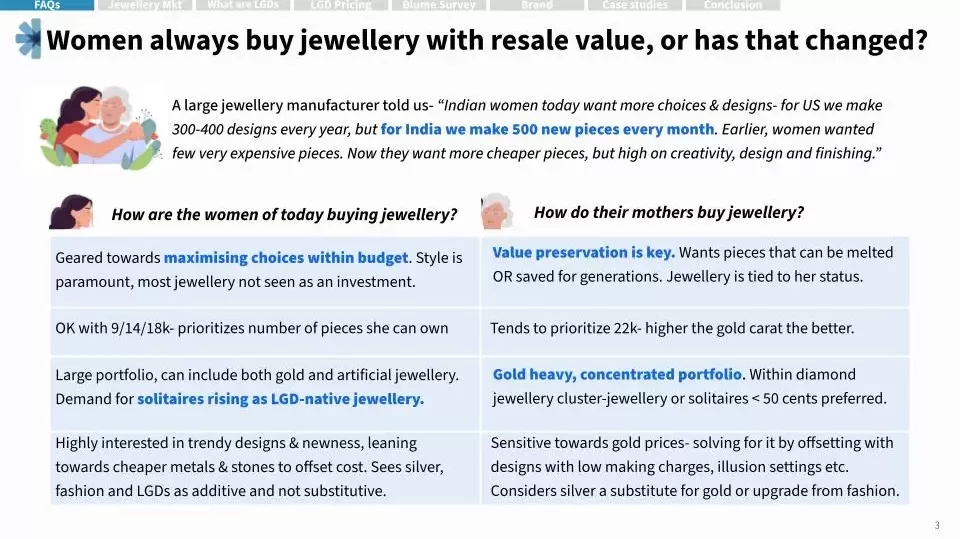

For decades, Indian women bought jewellery for value preservation. They wanted 22k gold pieces that could be melted or saved for generations, tied to status and investment. Within diamonds, they stuck to cluster jewellery or small solitaires under 0.5 carats.

Today’s consumer thinks very differently. She’s maximizing choices within budget, prioritizing style over investment value. She’s comfortable with 9k/14k/18k gold and owns a mix of gold, silver, fashion jewellery and increasingly, LGDs. She sees these as additive, not substitutive. A large jewellery manufacturer told us: “For the US, we make 300 – 400 designs every year, but for India we make 500 new pieces every month.”

The meaning of “diamond” is shifting. LGDs make solitaires 80 – 90% cheaper, moving what was aspirational into everyday territory. A 1‑carat stone isn’t just an engagement ring, it’s a birthday gift, workwear, or a self-purchase you don’t need to justify. One consumer summed it up: “I didn’t have to rethink my life. It didn’t break the bank.”

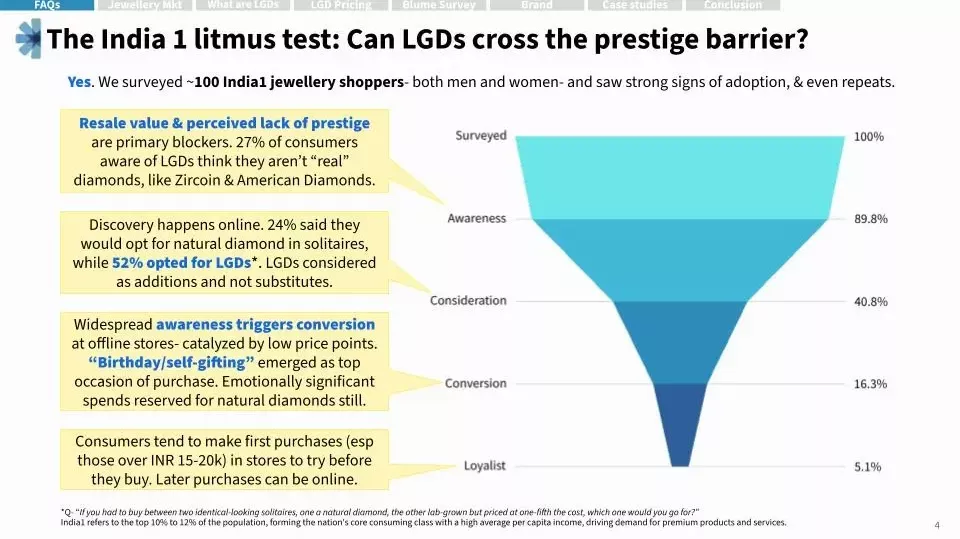

Our survey of ~100 India‑1 buyers shows awareness is high (90%), but consideration drops to 40% due to concerns around prestige and resale value. Once consumers cross that barrier, conversion is meaningful (16%), and a small but notable loyalist base (5%) has emerged, showing early repeat behaviour. What surprised us most? Self-gifting emerged as the top occasion, while old as a concept, we see this as a growing trend amongst 30+ women.

The Big Skepticism: “Won’t Prices Keep Falling?”

This is the question we hear most. If LGDs are getting cheaper every year, won’t they become commodities?

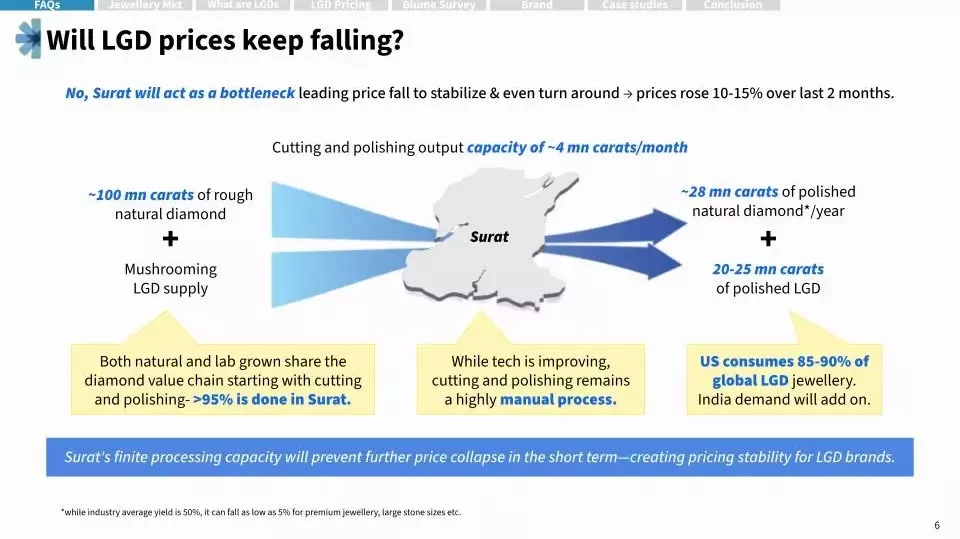

Our view: No. LGD prices have fallen since 2018, but not because demand collapsed. Early margins were inflated. What we’re seeing now is margin normalization, not commoditization.

The real constraint isn’t growing diamonds, it’s cutting and polishing them. Nearly 90 – 95% of global diamond cutting happens in Surat. This capacity is finite, highly manual, and shared between natural and lab-grown supply chains. While new players can start growing with entry-level CVD machines (₹30 – 50 lakh), high-quality production remains concentrated among legacy growers who’ve spent years and thousands of crores perfecting yield and clarity. One grower told us: “Each seed is different. We developed our own processes for these.”

The US already absorbs 85 – 90% of LGD jewellery, and India’s demand is just beginning. The system doesn’t have the throughput for endless deflation. In fact, prices have risen 10 – 15% over the last two months. The floor is forming.

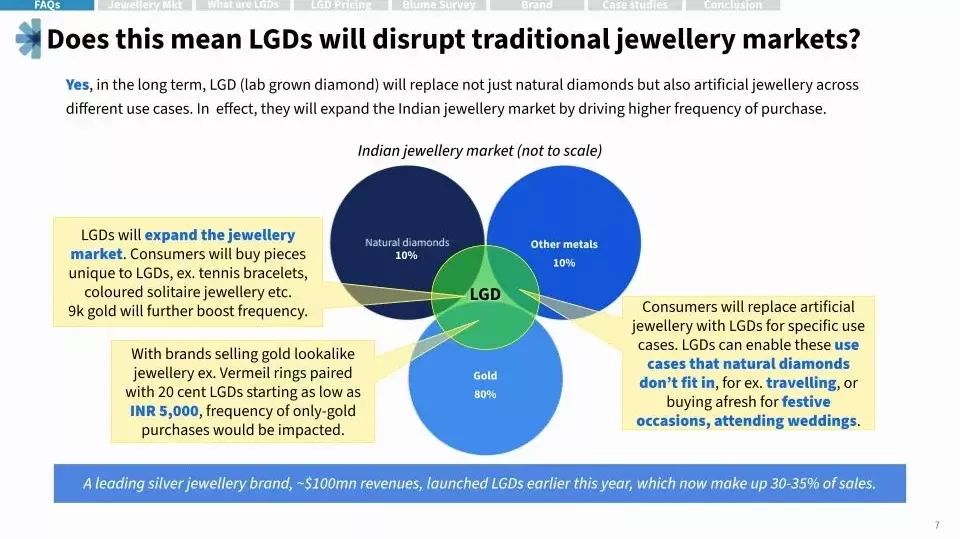

LGDs Aren’t Replacing Diamonds, They’re Expanding the Market

Consumers are replacing artificial jewellery with LGDs for travel, festivals, and weddings. They’re buying entirely new formats like tennis bracelets and coloured solitaires that were never economically viable with mined diamonds. And lower price points in 9k-gold LGD jewellery (₹5,000 – ₹15,000) are creating new, more frequent purchase moments for traditional gold buyers.

For existing buyers, LGDs unlock real optionality. They upgrade quality within the same budget (VS2 natural → VVS LGD) or jump significantly in size (0.2ct natural vs. 1.5ct LGD at ₹25,000). One consumer told us: “In natural diamond, I won’t get the best clarity for 1 carat. In LGD, I get VVS1 for ₹85k. The same at Tanishq would be ₹4L.”

LGDs sit at the intersection of diamond, gold, and artificial jewellery use cases, unlocking entirely new behaviour and higher buying frequency.

The Incumbents Are Betting Long-Term

One of the strongest signals for LGDs is legacy jewellers entering the space. This is almost always through separate brands. Tata launched Pome under Trent, not Tanishq. Senco launched Sennes. Goldiam launched Origem. A large public jewellery co has invested in a young LGD brand, indirectly entering the space.

This shields their mined-diamond equity while addressing value-conscious purchases for the same or different consumers. When incumbents build new brands for a category, it signals long-term belief, not experimentation.

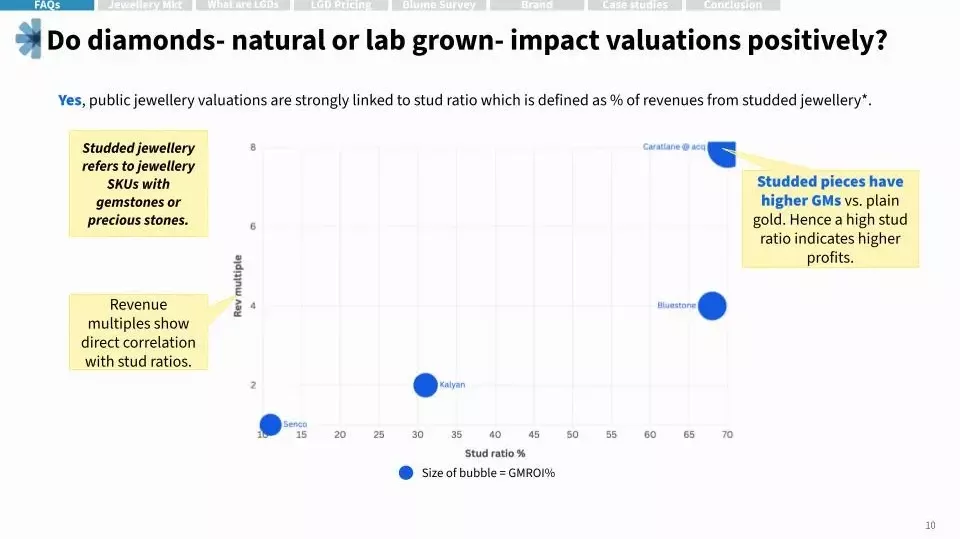

And this matters for valuations. Public jewellery companies with higher stud ratios, whether natural or lab-grown, consistently command better multiples. CaratLane and Bluestone (60 – 70% studded jewellery) trade at 6 – 8x revenue. Kalyan and Senco (11 – 28%) sit at 1 – 3x. Why? Because studded pieces carry much higher gross margins than plain gold. LGDs give brands a way to build stud ratio at scale.

The Stories That Shaped Our Thesis

To validate this, we surveyed ~100 India‑1 buyers, interviewed a dozen LGD consumers, and spoke with retailers, manufacturers, growers, and legacy miners. What stood out wasn’t just the data, it was the ability of LGDs to create a buzz: the confusion around “real or not,” the excitement of buying bigger stones for self-gifting, the rise of “daily wear diamonds.” One 32-year-old said: “I went to the store out of curiosity. The prices were low enough that I could buy impulsively. I just wanted it.”

We also studied brands that scaled globally around a single material or format — Swarovski with crystals, Pandora with charms, Brilliant Earth with engagement rings. Across all these, focus won over breadth.

So Where Do We See Opportunity?

In brands that understand LGDs aren’t just “affordable natural diamonds”, they’re a new design canvas, occasion set, and consumer behaviour. In retail formats that balance online discovery with offline trust building. In supply chain plays that leverage India’s cutting and polishing dominance.

The Category is Still Early But the Fundamentals Are Real

Natural diamonds aren’t going away. The emotional equity around rarity is too strong. But we believe natural and lab-grown will coexist and LGDs will expand the pie, not just take share. Natural diamonds will remain tied to life’s biggest moments. LGDs will fill the in-between: birthdays, self-gifts, travel jewellery, pieces you wear to work.

In this thesis, we unpack how consumers are changing, how supply works, how brands are positioning themselves, and where we see long-term opportunity across the LGD stack.

The category is still early. Consumer perceptions are forming. Brand narratives are being written. But when both behaviour and economics align, that’s usually when things get interesting. And right now, in lab-grown diamonds, we think they are.

Authors

Apurva Dixit

Apurva looks after all things “consumer” at Blume. She’s been in several consulting roles at Big 4s and ran her own business as a banker for early stage startups.She is an angel investor and believes passionately in the founders…- Current Section

- Vice President, Investment

- Sector

- ConsumerTech

Muskan Gupta

Muskan supports the Consumer investments practice at Blume. She is a graduate of BITS Pilani, holding a degree in Electrical and Electronics, with a strong passion for startups and innovation.Muskan brings diverse experience from…- Current Section

- Analyst