The New Era of P2P Lending

- Published

- Reading Time

- 8 minutes

- Contents

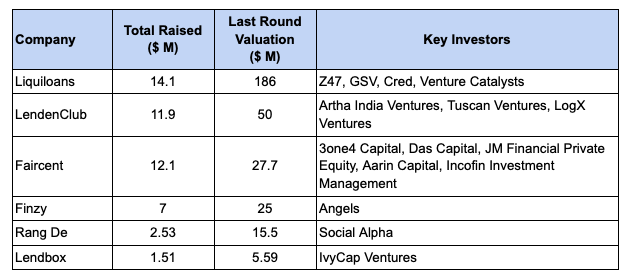

India’s P2P lending ecosystem has come a long way, with estimates pointing at ~₹20,000 crore in disbursements. The country now has 26 licensed NBFC-P2Ps, with many raising significant capital to build offerings, such as Faircent, LenDenClub, Lendbox, and Liquiloans.

Select P2P NBFC funding Source: Traxcn

RBI has held a cautious approach to P2P lending given the massive upheavals it has seen in other ecosystems such as China. Instead of taking a reactive approach to blanket ban such financial instruments, it has taken a proactive approach to regulate the industry with guidelines from its nascency. These guidelines have involved approving a new type of NBFC license specifically catered towards P2P, allowing registered intermediaries to act as the platform for facilitating P2P credit from individuals.

Unlike traditional lenders such as banks and NBFCs, their role is not to disburse capital from their balance sheets but only to facilitate P2P transactions and make revenue from platform fees, which they charge to investors and borrowers, or so was the expected behavior. The RBI had also gone ahead to protect exposure risk among investors by setting upper limits on maximum exposure towards the overall P2P ecosystem, capping it at ₹50 Lakhs in aggregate across platforms and for anyone looking to lend over ₹10 Lakhs through P2P platforms needs to provide a net worth certificate by a chartered accountant certifying a minimum net worth of ₹50 Lakhs.

These guidelines, though already seen to be forward-looking, paved the way for P2P NBFCs to launch an exciting new “investment” product that had defined gains and liquidity for investors over shorter tenures, combining the best of both worlds in terms of the rudimentary operating mechanisms of the defined term-linked returns of fixed deposit and the liquidity of a mutual fund. With the added benefit of facilitating borrowings, fintechs partnered with such NBFCs to offer a new investment and borrowing product for their users, thus gaining popularity for P2P products. Many large fintechs, such as Cred and BharatPe, actively marketed such products and ultimately built a strong pool of investors and borrowers.

It was particularly a source of easy credit for risky borrowers as these P2P NBFCs could promise a return of 8 – 12% for investors while usually charging upwards of 20% interest to its borrowers, creating a healthy spread that can be used to generate further revenue while keeping NPAs financed. This made an optimal arrangement for P2P NBFCs, too as it could help guarantee returns to its investors.

However, positioning P2P lending as an investment product was an innovator’s interpretation of fintechs and P2P NBFCs on the true intent of the RBI’s guidelines, which the regulator has now acted upon.

Clearly, the rationale behind clarifying and amending the regulations has been that of protecting the retail customer. On the borrower front, P2P platforms had the allure of easy borrowing as the NBFC’s capital was not at risk but a pool of lenders, allowing the NBFCs to charge high interest rates and fees to benefit from borrowers. On the lenders’ side, the allure of higher-than-FD returns at shorter tenures made them excited about P2P products, exposing them to significant credit risks, as in the true spirit of the guidelines.

The perceptibly harsh guidelines championing consumer protection have shaken up the entire P2P ecosystem, fundamentally altering the most shiny bits for lenders, borrowers, and platforms.

The key changes have been summarised below.

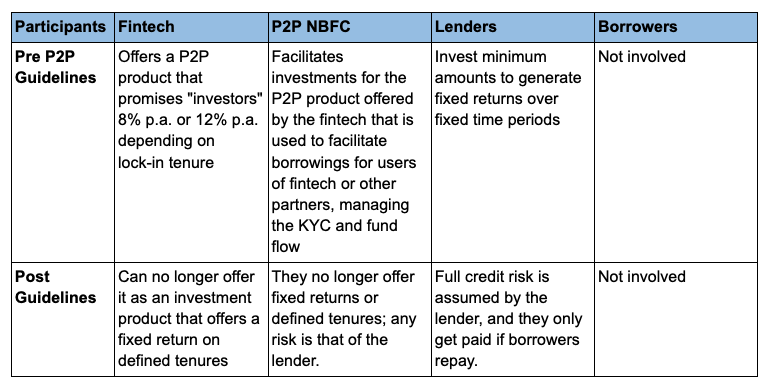

P2P is a credit product, not an investment product

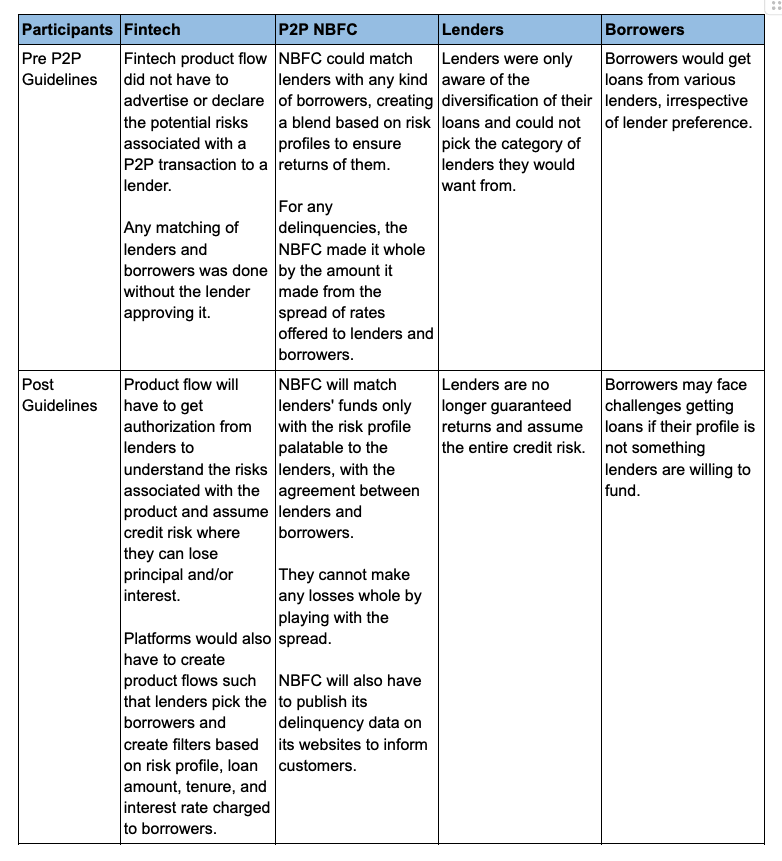

The regulator has clarified that P2P instruments are not investment products, and platforms cannot offer tenure-linked fixed returns or instant liquidity to lenders (creatively called investors by platforms). As a result of this clarification, it has also gone on to mention that P2P NBFCs are mere facilitators of such transactions. The entire credit risk of the principal and any interest needs to be borne by the lenders of the platform, with the understanding that they may stand to lose the entire principal and interest should a borrower not repay.

P2P products can no longer be treated as a mutual fund where one can park their funds and let them grow over time. P2P NBFCs facilitated this by rolling over borrower repayments to new borrowers whenever the loan tenure ended. This made it appear to lenders that their funds were constantly growing with little to no deviation from the promised returns.

A credit product sounds much less exciting for a retail consumer looking for a new” investment” product for sure.

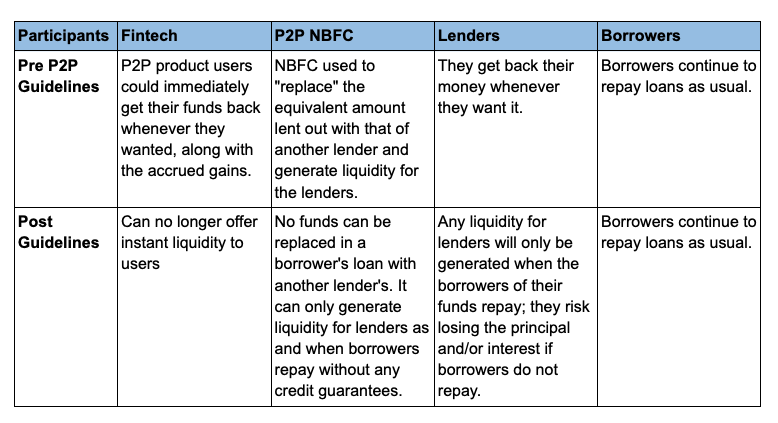

No more instant liquidity or premature withdrawals for investors lenders

P2P products had seen a massive uptick in adoption, for they offered instant liquidity to lenders of the platform while still assuring annualised returns. P2P NBFCs facilitated this practice by replacing the funds lent by one lender with that of another, generating liquidity for those who wanted it, akin to a secondary market transaction.

This practice has explicitly been prohibited, thereby blocking any products that offered instant liquidity without any lock-ins to the lenders. The lenders can only see returns of their capital along with any interest on the repayment of such loans by a borrower and over the course of the loans’ tenure.

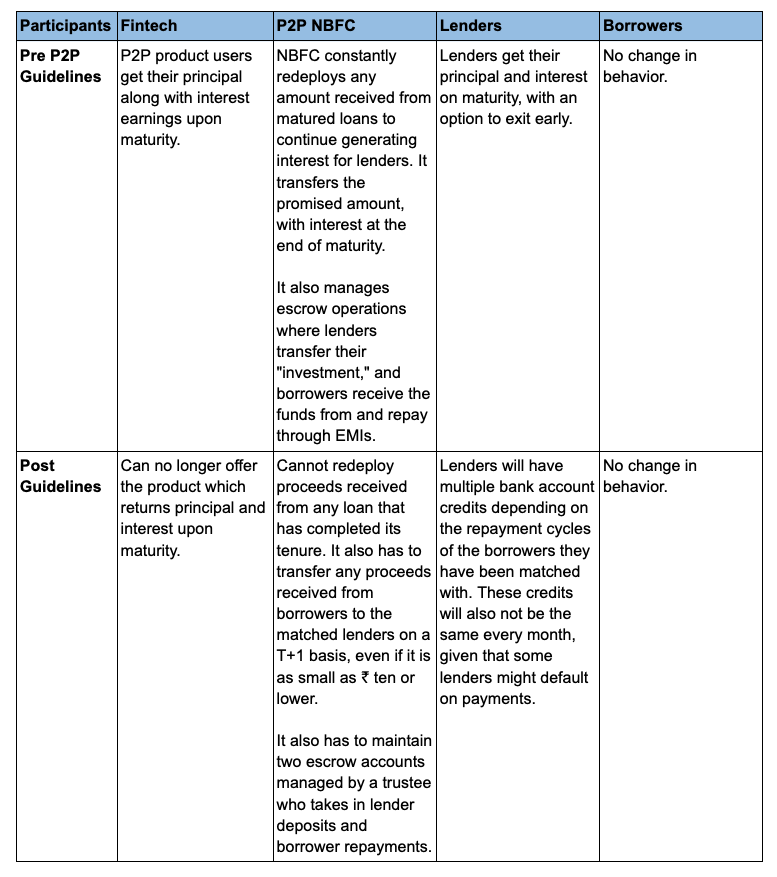

Time limits on settlements of proceeds received from lenders and borrowers

Most P2P NBFCs earlier used to operate one escrow account to take in lender deposits and borrower repayments. With the new guidelines, RBI has clarified that P2P NBFCs need to operate through two trustee-managed escrow accounts — one to take in lenders’ money for disbursals and another to collect borrowers’ repayments.

However, there was no specific time limit for the settlement from borrowers to lenders or vice versa. The RBI has now clarified that any such settlements with the lenders or borrowers should happen on a T+1 basis.

This means that the earlier practice of P2P platforms using repaid amounts from borrowers to re-deploy to a new set of borrowers to generate higher returns for lenders is no longer permitted. This also means that the operational heavy lifting that P2P NBFCs will have to perform will also increase. P2P lenders used to diversify as little as ₹10 from a lender into a basket of loans to help lower risk. This means that a lender’s ₹10,000 deposit can be spread over 1000 loans with differing interest rates and repayment schedules. With this change in regulations, P2P NBFCs have to significantly overhaul operations to ensure that repayments across 1000 loans with amounts as little as ₹ ten are transferred to the lenders’ accounts through the trustee-managed escrow system on a T+1 basis.

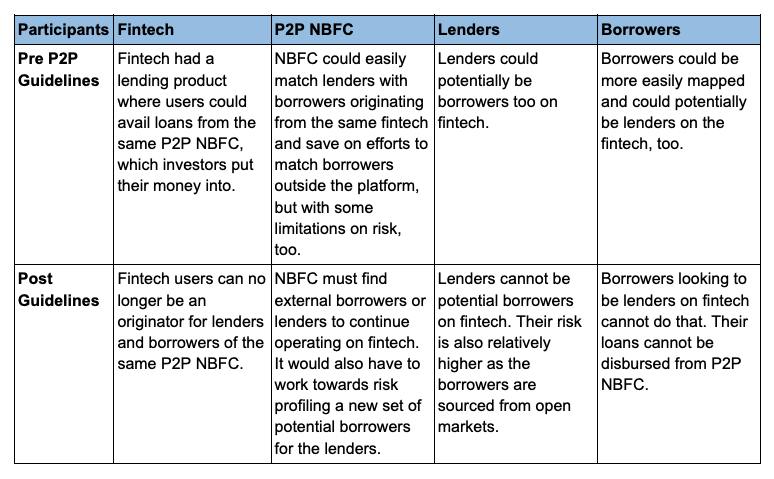

No more closed-loop transactions

P2P NBFCs benefitted from partnering with fintechs for distribution because they helped on the two fronts of this business — finding a sizable pool of lenders and an even more sizable pool of borrowers — thereby creating a closed ecosystem specific to the fintech platform. The operational overhead of mapping lenders with borrowers was significantly lowered through such partnerships.

However, the RBI has very clearly said that such closed-loop transactions are not allowed. All P2P NBFCs now have to create a distinct mapping of lenders and borrowers through open markets and board-approved policies where it can either be a lender or a borrower partnership through fintechs. This would also impede the revenue potential of offering a closed-loop product, with fintechs only being able to capitalize on one leg of the transaction rather than the entire transaction value chain.

Consumer protection at the forefront

While P2P was marketed as an investment product, consumers on the lender side seldom understood its risks. With the new guidelines, it has been made abundantly clear that P2P NBFCs are facilitators of the transaction and would assume no risk arising from non-repayment of principal or interest by borrowers, i.e., lenders do stand the risk of losing their entire capital in the process.

Any lender now would be made adequately aware of the risks associated with the transaction through declarations that they see in the product journeys of P2P transactions. More so, lenders would now have to approve any borrowers and be made adequately aware of the risk profile, loan amount, interest rate, tenure, and other details associated with the transaction. The loan agreement, too, would be between the lender and borrower, facilitated by the P2P NBFC. Any return of their capital will only materialize on repayment by borrowers and would have to be associated with the tenure of loans rather than the earlier defined returns over a fixed period.

All NBFC-P2Ps would also have to publish monthly data on their portfolio to aid informed decision-making for consumers. However, there is no standardized definition that the RBI has placed on NPA and delinquencies, which still allows room for muted delinquency data.

NBFC-P2Ps would continue to facilitate loan recovery services, but this does not mitigate the risk of capital loss.

A fundamental shift in the P2P NBFCs business model

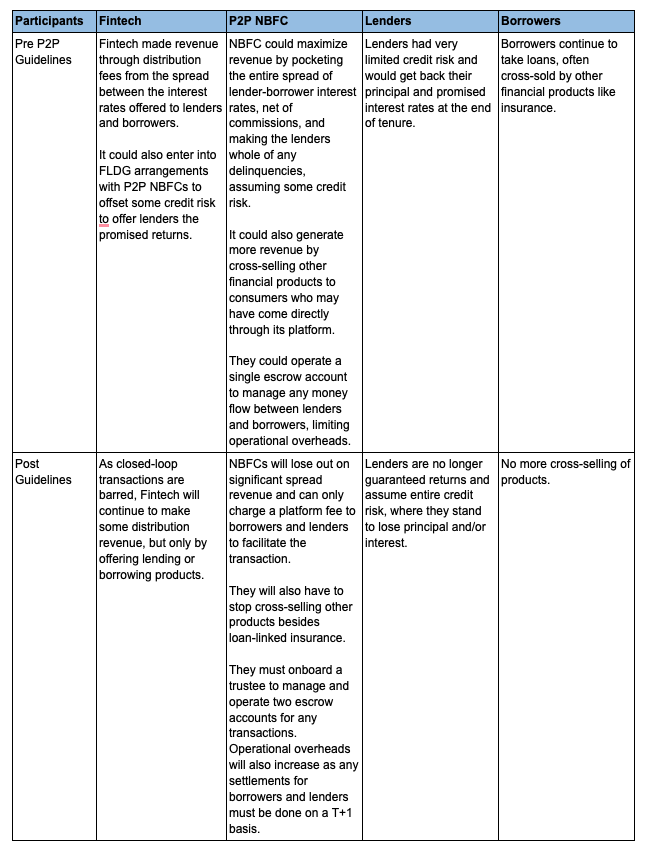

Early last year, through the FAQs on digital lending guidelines, the RBI made clear that FLDG arrangements would not be permitted for NBFCs in the P2P class. This had made it shrunk promises of higher returns that P2P platforms had offered through fintech partnerships and led to a bloating of NPAs.

Credit guarantees provided by P2P NBFC partners had a risky connotation to it. They offset the actual delinquent behavior of borrowers on the platform, painting a much better picture for the NBFCs on their NPA numbers. The existing provisions of the digital lending guidelines, coupled with the new P2P lending guidelines, will show the true picture of delinquencies on these platforms, and the ultimate retail consumer is the one who is responsible for all the risks associated with a transaction.

With the new guidelines published, it has further gone on to mention that P2P NBFCs can only charge a platform fee as a fixed amount or a percentage of the lenders’ amount. This is a deviation from the norm where P2P NBFCs could pocket the spread between promised returns to lenders and the rate of interest charged to the borrowers, net of any commissions paid to its partners, and any losses it needed to make whole as part of offering fixed returns.

With the entire risk and reward being transferred to the lenders of the platform and the increased overheads coming from T+1 transaction processing as well as the ban on closed-loop lender-borrower mapping, P2P NBFCs are sure to feel the squeeze.

A final nail in the coffin for P2P platforms is the restriction to cross-sell any products apart from loan-linked insurance products. Cross-selling plays a major role in growing the business for financial services platforms by unlocking ancillary revenue streams and growing margins beyond what the core product can generate, even at full scale. For P2P platforms, while it was earlier cozy to make a spread from lenders and borrowers, the restriction to only charging a platform fee and the cross-sell ban, any margin expansions that P2P NBFCs could have thought about are now halted from the get-go.

The RBI has constantly monitored the P2P space hawkishly and has conducted multiple audits at P2P NBFCs to understand the ecosystem better. With these guidelines it has altered the space altogether. While consumer protection is at the forefront of these guidelines, the allure that P2P products offered to lenders is now gone, with no risk-adjusted returns, defined tenures, or instant liquidity. These changes might as well signal the end to a glorious run for these products but would also allow for good actors in the ecosystem to work alongside the regulations to build products that do good by the consumers and continue to retain trust.

Links:

Author

Akshat Praneet

Akshat works closely with Ashish Fafadia on navigating strategy for Blume's growth portfolio companies and supporting on the fund's DPI efforts. Prior to Blume, Akshat explored the operator side of things at Jar…- Current Section

- Senior Analyst, Strategic Planning

Reports

Building Agritech for India | Agritech Bluprint

India's agricultural sector, a cornerstone of the nation's economy, is on the brink of a transformative revolution powered by technological innovation and digital solutions. As a global leader in the production of various…- Current Section

- Report

- Authors

- Ashish Fafadia, Jatin Madhra

- Published

India InsurTech Bluprint

The Indian insurance sector is rapidly evolving, driven by significant regulatory changes and technological advancements. With the country's insurance market expected to triple in size by 2032, there is substantial…- Current Section

- Report

- Sector

- FinTech

- Authors

- Ashish Fafadia, Jatin Madhra

- Published

Commentaries

The Inside Scoop on "Fintechs and IPOs": Takeaways from Blume Fintech Summit

India isn't just catching up in the fintech race; it's leading the pack. With a staggering fintech adoption rate of- Current Section

- Commentary

- Authors

- Jatin Madhra

- Published