Decoding Exit Patterns in the Indian Startup Ecosystem | Blume Ventures’ Perspective

Originally shared as a part of the quarterly update with our Limited Partners, this analysis of exit patterns in the Indian startup ecosystem garnered significant interest and prompted thoughtful discussions in our networks. As a result, we decided to make our take available to everyone as we continue to champion much-needed transparency and knowledge sharing in the venture/startup ecosystem. This nuanced overview of exit strategies — covering Secondaries, M&A, and IPOs — draws from our extensive experience as investors, having seen the ecosystem grow over the last decade and more. I hope you enjoy reading it and it helps you build a better understanding of how venture funds operate. You should think of it as V1; we’ll be unpacking more about venture fund exits in India in the next few months.

As seasoned participants in the Indian startup ecosystem, we are all well aware of the perennial questions around the critical role of exits in a fund’s lifecycle. If one has attended our Blume Days, there’s always a main stage conversation around the exit topic, understanding what it takes to go public, celebrating M&As inside the portfolio and outside of it. This year, we brought every one of the 17 largest exits from Fund 1 / 1A on stage and celebrated them in a final nod to their 4x+ fund outcomes that they helped deliver.

In this edition of the LP newsletter, we aim to further provide a nuanced overview of exit strategies for venture funds in India.

We unpack three types of exits: Secondaries, M&A, and IPO. We have analyzed the Blume portfolio data and also noted the parallels of key exit events in the Indian startup ecosystem. We hope this commentary and the charts will expand the horizons of exit frameworks for observers and participants in the Indian ecosystem.

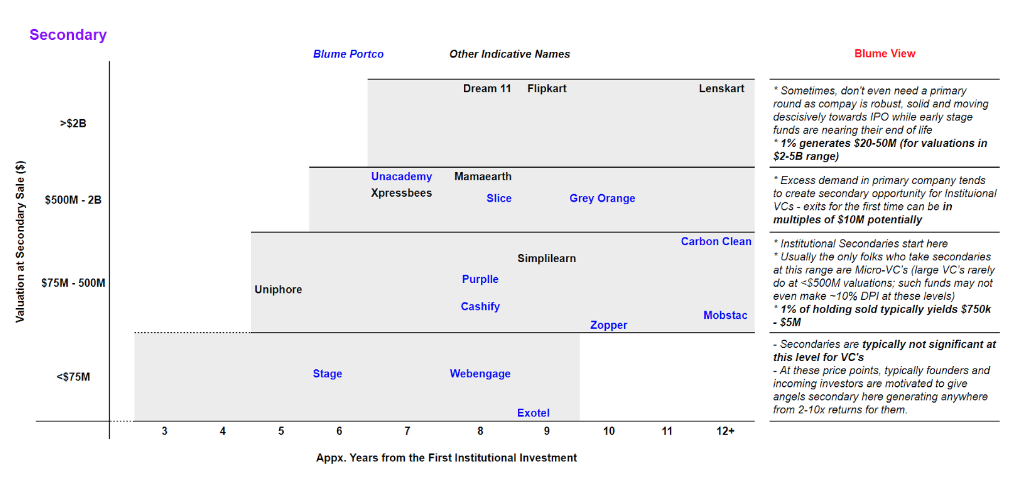

Secondaries

Secondaries enable funds to generate liquidity / DPI (fund term for “Distributed to Paid In” capital, i.e., % of the capital that’s been returned back to investors e..g. If the principal is returned inclusive of fund fees, one would say 1.0x DPI) without waiting for an M&A or IPO. A fund’s participation in secondaries, IF at all a secondary opportunity is available, depends on how much the secondary moves the DPI needle. Generally, funds don’t sell unless the return can make at least 10% DPI i.e.10% of the fund corpus. Therefore, secondary sellers exercise this option if there is demand for the startup’s shares whenever it materializes at different stages of a company. Angels take exits first — quantum and % ownerships are very small and insignificant outlay to the company and the new institutional buyers (relative to sizes of even smaller Series A/B/C rounds) but can be a significant multiple to the angels’ principal amount. MicroVCs follow when companies scale a bit more, and then larger institutional funds like Blume Ventures may seek a meaningful part exit (usually, it’s always a part exit for larger shareholders) at >$500M valuations.

Most secondaries in the first 4 – 5 years of a company occur at a sub $75M valuation, generally unattractive for institutional VCs. These are instances of founders and incoming investors consolidating the captable by providing liquidity to early angels, who get 2 – 10x returns.

The $75-$500M valuation bracket marks the start of institutional secondaries. A 1% holding can yield $750,000 to $5M cash returns, making it a sweet spot for micro-VCs. However, it is usually unattractive for large funds as the returns are much smaller as a % of their fund size. When one looks at Blume’s exits from Mobstac, Purplle, Zopper, etc., please note that these were game-changing returns for a $20M micro-VC that was Blume Fund I. Similarly, a Boat and MamaEarth (for Fireside), a Whatfix and MamaEarth (for Stellaris) and Purplle (for IvyCap) were stellar part exit outcomes for funds which were all <$100M in size. The % of DPI for the same franchises in their next funds, at the same valuation points, would be much lower (since their funds grow 2 – 5x in size from their first funds). This is true for Blume’s exits too.

The $500M to $2B range is the prime zone for institutional VCs to begin getting secondary exits, as excess demand in primary funding rounds for these break-out companies creates secondary opportunities. Institutional funds can potentially achieve exit values in multiples of $10M or more, which usually appear after the 7th or 8th year of writing the first check.

For companies over $2B, a 1% stake can yield $20 – 50M in secondaries (as would be the case with Lenskart’s secondaries at a $5B valuation). These companies are typically cash flow positive or trending towards EBITDA/PAT profitability and heading towards an IPO. Secondaries at these price points usually occur between the 7th and 12th year, when the early-stage funds (most of which are nearing the end of life) have an opportunity to generate significant returns.

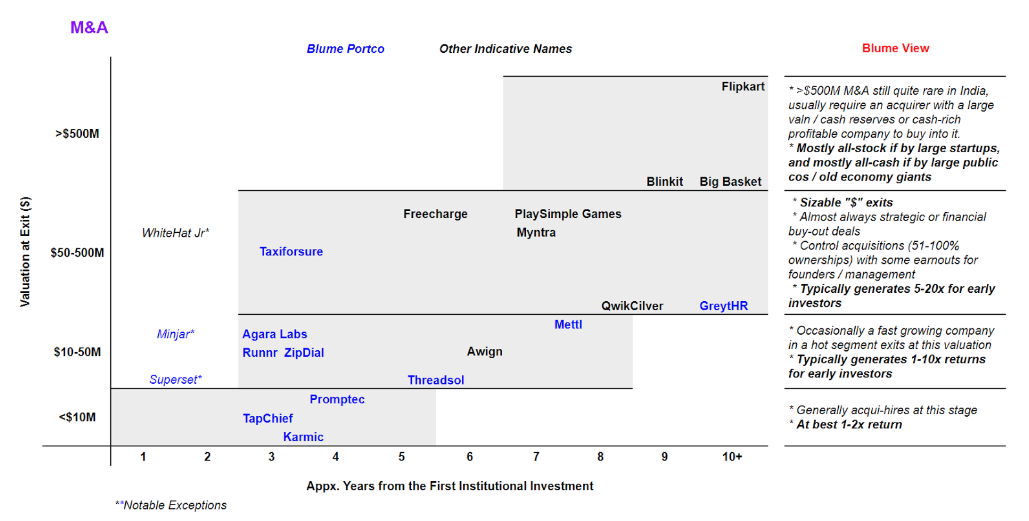

M&A

M&A exits generally follow a pattern, with rare exceptions. Large dollar exits ($50M to $500M) usually occur between years 3 to 8 of a company’s lifecycle as a majority buyout by a financial or strategic investor. Super-large M&A outcomes ($500M+) are rare, and only acquirers with large captables or massive cashflow can afford these acquisitions. The most notable large M&As since the VC era began have been led by the legendary Walmart-Flipkart one, followed by Tatas picking up Big Basket, 1Mg, CaratLane, and Prosus-group led M&A (ibibo to MMT, Redbus prior to that and CitrusPay by PayU, apart from the near miss BillDesk offer).

Most M&As in India within 5 years after the first institutional check occur at sub $10 – 20M. These are typically acqui-hires, yielding just offers for employees or at best 1 – 2x returns for early investors. At Blume, we have had a few dozen of these over the 13 years.

The second category is $10-$50M M&As. These exits also typically occur between years 3 and 8 post investment and generate 1 – 10x returns on seed checks. Blume portfolio examples include companies like Runnr (to Zomato), ZipDial (to Twitter), and Mettl (to Mercer Consulting). Occasionally, a fast-growing company in a hot sector will provide a quicker exit in this range.

The $50M to $500M range of exits provides sizable dollar exits to seed and perhaps even Series A funds. These deals almost always involve a financial or strategic investor taking control by buying out the majority stake. In most cases, seed investors exit with 3 – 20x returns. Examples include Blume portfolio’s TaxiForSure (to Ola) and non-Blume companies like Freecharge (to Snapdeal), Myntra (to Flipkart), and WhiteHat Jr (to Byju’s).

As mentioned above, India has seen only a handful of M&As beyond the $500M mark. In each case, the deal occurred much later in a company’s lifecycle, and the acquirer either had a large valuation, cash reserves, or massive free cash flows. Blinkit’s acquisition by Zomato is turning out to be one of the fastest value-accretive acquisitions in the Indian market.

IPOs (or Going to the Public Market)

IPOs are the best exit outcomes for founders and venture investors in India, potentially generating sizable cash returns for the fund. IPOs follow a few distinct patterns in India.

The entry barrier for an IPO is lower than believed. Companies like Tracxn and Unicommerce (listing at approx INR 1000cr / INR 10B; USD $120M) have shown that the public market has a huge appetite for profitable/close to profitable tech companies with even as little $10 to $20M in revenue. Companies can list on the main board at the BSE/NSE for as little as $100 to $300M in initial market cap, providing sizable returns to investors and allowing for founders to compound as impressively in the public market as would’ve been expected in the private market. More importantly, when the company reaches this path, there is a sudden surge from PE players (mid-market PEs for small-cap listings and even large PEs for mid-cap listings), pre-IPO funds, secondary funds, and the choices and scope for liquidity multiplies relative to private market options. The catch is the strong need for a path to profitability, if not already there, combined with robust growth options in revenues and margin structures.

Even smaller companies with $4 – 5M in revenue can list on the SME exchange. Blume Fund I company E2E Networks listed within 8 years of our seed investment and grew into the main board and is thriving now, well beyond our full exit. Infollion (also Blume Fund I) emulated them in 2023.

IPOs beyond the $300M market cap usually occur 8 to 10 years into a company’s lifetime, with the $1B+ market cap reserved for market leaders. The beauty of the Indian public market is that even if you are not profitable at listing, if you deliver on your promise to become profitable, you’ll be handsomely rewarded. For instance, Zomato saw a surge in its market value once it delivered on its path to profitability promise. Others are following this trend set by early movers like Infoedge, Nazara, Rategain, and IndiaMART in their respective categories and sizes.

We expect the deluge of path to public companies to continue. The market is seeing plenty of issuances from companies born in the first cycle of 2007 – 15. We expect many of the venture-backed new businesses to follow this path. Between SME, small, and mid-cap IPOs, we are still on course to see the numbers swell from <10 in 2020 to over 50 by Dec 2025. Ixigo, FirstCry, Ola Electric, Unicommerce, and more are all IPOs from just this past quarter.

As our analysis demonstrates, the exit landscape in India is far more nuanced than often portrayed. We hope our note helps unravel the growing possibilities and options for exits by the year. Ultimately, the key to success in the Indian venture market lies in understanding these nuances of the exit markets, maintaining patience, and strategically positioning investments to capitalize on the most suitable exit opportunities sooner than later.

The data presented in the charts and referenced in the article is derived from a blend of internal Blume data (specific to Blume portfolio companies) and external sources such as Tracxn, Pitchbook, and others.

Author

Karthik Reddy

Karthik Reddy is the Co-founder and Managing Partner at Blume Ventures, one of India’s leading early-stage venture funds with over US$900 million in AUM. Blume invests in emerging tech and tech-led innovation from Seed to Series A…- Current Section

- Co-founder & Partner

- Sector

- Media, Entertainment & Gaming, ConsumerTech

Commentaries

Beyond Unicorns: E2E Networks and Alternative Paths to Stakeholder Value Creation

In India's startup ecosystem, the path to success is often portrayed as a journey with just one end goal: achieving unicorn status and then maybe pursuing a multi-billion dollar IPO. This narrative,…- Current Section

- Commentary

- Authors

- Vikram Gawande

- Published

The Omega Files - The “Why did you do it?!” Question | Part 1

The article, "The Omega Files: The Why? Part I," presents insights from the Blume team on the rationale behind their decision to publicly release the Omega Files. It includes varied perspectives from the leadership and investment team,…- Current Section

- Commentary

- Authors

- Karthik Reddy

- Published

PART I: Keep Calm And Go All The Way To The IPO Bell (At Least In Your Head)

Every year, for the past 8 years, I have got the same question a few minutes into every LP meeting (LPs or Limited Partners are the financial investors who give funds such as Blume the capital to invest into startups). “Where are…- Current Section

- Commentary

- Authors

- Karthik Reddy

- Published

Reports

The Omega Files | Episode 1

Blume Fund I Declassified- Current Section

- Report

- Authors

- Karthik Reddy, Adithya Santhosh

- Published