The Silicon Playbook

- Published

- Reading Time

- 1 minute

- Contents

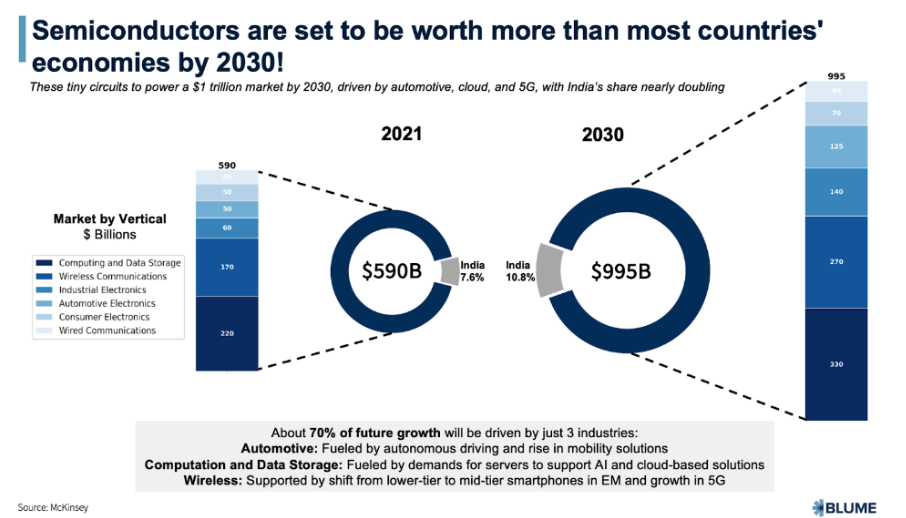

Imagine, for a moment, a world without semiconductors — no smartphones, no internet, no self-driving cars, not even the humble digital toaster. These tiny silicon chips have quietly transformed from niche technical components to the heartbeat of the global economy, accounting for around 1% of global GDP. As we rush toward a future full of AI, electric vehicles, and smart devices, semiconductors are poised to become even more critical.

Resource

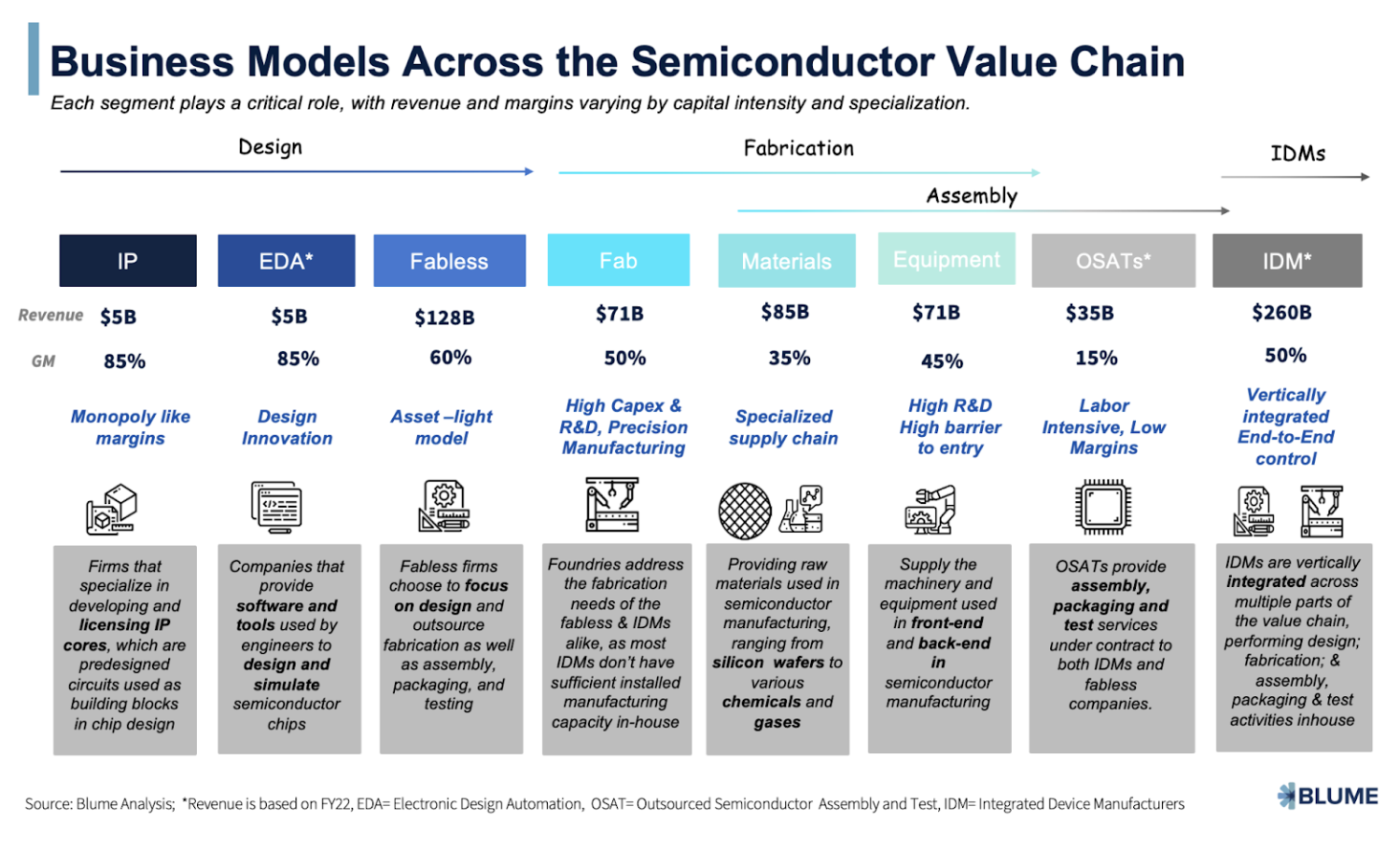

The semiconductor ecosystem is diverse, with business models shaped by capital intensity, R&D needs, and specialization. The big players fall into a few key categories:

- Integrated Device Manufacturers (IDMs): Think Intel or Samsung. These giants design, manufacture, and sell their chips. With a 50% gross margin, IDMs require high capital for in-house fabrication and control end-to-end processes.

- Foundries: Companies like TSMC and GlobalFoundries don’t design chips but fabricate them for others. Foundries tend to serve fabless design-focused companies that outsource their manufacturing. High CapEx is par for the course, with returns on precision manufacturing as these businesses work with demanding clients.

- Fabless Companies: Here, companies like NVIDIA and Qualcomm shine, designing groundbreaking chips and leaving manufacturing to foundries. This asset-light model allows them to keep gross margins high — about 60% — while focusing on R&D and innovation(SemiCon_Final_Deck).

- OSATs (Outsourced Semiconductor Assembly and Testing): This sector performs assembly and testing, adding low margins but providing a vital link in the chain.

IP Providers: These firms develop intellectual property blocks — like pre-designed circuits for specific functionalities — that designers can license. Licensing and royalties mean these firms enjoy “monopoly-like” profit margins, operating with nearly 85% gross margins.

The pandemic-driven supply chain crises exposed a geographic mismatch between chip production and demand hubs. With 75% of semiconductor manufacturing concentrated in East Asia, the United States, Europe, and India seek to de-risk this dependence on China and Taiwan, with governments earmarking $380 billion in incentives. India, for instance, seeks to capture 11% of global semiconductor demand by 2030, by investing in fabs and assembly plants that could bolster the nation’s position as a supply chain stabilizer.

The Grand Challenges and Opportunities: What’s Next for Semiconductors?

Let’s dive into what might drive the next semiconductor wave:

- AI and Advanced Chip Design: AI demands are pushing for chips with massive processing power. As AI models become more complex, AI-specific chips like AI accelerators and neuromorphic chips are fast becoming critical for training and running these models efficiently.

- Advanced Materials: Silicon has ruled semiconductors for decades, but new materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) can handle high voltages and frequencies, making them ideal for electric vehicles and renewable energy solutions. While silicon will not disappear, the era of GaN and SiC could bring about more efficient, powerful devices.

- Quantum Computing and Neuromorphic Chips: Quantum computing, once science fiction, is now edging into reality with experimental applications. These machines rely on qubits, which exist in superpositions, to solve complex calculations in minutes rather than years. Meanwhile, neuromorphic computing mimics brain architecture for efficient, low-power AI processing, a potential game-changer for autonomous robotics and large language models.

- Semiconductor-Biotech Hybrids: Known as “SemiSynBio,” this emerging field blends biology with semiconductors to create energy-efficient, high-density data storage systems. DNA-based storage or biological sensors could redefine data storage and computation, shifting the tech landscape from silicon toward biological hybrid solutions

The Indian Semiconductor Scene: A Market Ripe for Growth

India’s semiconductor market — worth around $50 billion in 2021 — could more than double by 2030. The country’s existing talent pool in chip design (boasting over 125,000 experts) positions India as a fabless design powerhouse. However, production lags: only 9% of components are locally sourced, with many designs sent abroad for testing and manufacturing. This makes fabless and ATP (Assembly, Testing, and Packaging) promising business models for India, with room to expand capabilities through government incentives and private investments.

The government’s “Maruti 800” moment — a $10 billion stimulus to jumpstart fabs and component manufacturing — indicates a serious commitment. If successful, India could de-risk global semiconductor supply chains, marking its transition from a design hub to a semiconductor production heavyweight.

For an in-depth exploration, check out our comprehensive thesis here-https://docsend.com/view/gq46rc8mgts85dsc

Authors

Akhilesh Agarwal

Akhilesh Agarwal is an early-stage DeepTech investor who is passionate about supporting ambitious founders in their quest to advance humankind. He has spent over half a decade evaluating and investing in companies in various DeepTech…- Current Section

- Associate Vice President, Investment Team

- Sector

- DeepTech

Sonisha Kukreja

Sonisha joins the league of early tech investors at Blume hunting for radical thinkers in the EV, mobility & logistics, deeptech and healthtech domains. In her prior stint with Pravega Ventures, she looked at all things Fintech…- Current Section

- Analyst

- Sector

- ClimateTech, EV & Mobility, DeepTech, Healthcare